Nonprofit Financial Statements: The Complete Guide with Examples

Nonprofit financial statements aren’t just helpful – they’re required by the IRS. But did you know that they also build donor trust? In this guide, you’ll learn about the four key statements every nonprofit needs, how to prepare them, and which financial ratios are most helpful.

Nonprofits have a primary responsibility to the Internal Revenue Service (IRS) and their donors when filing and sharing financial statements. Nonprofits must file four statements every year to comply with IRS rules. Organizations must follow basic accounting practices when filing these statements and find ways to share these details in ways donors can understand.

Sharing these financial statements with donors is one of the best ways to ensure transparency and build trust.

In this article, we’ll explain more about each financial statement, why and when nonprofits need financial statements, and share examples of how organizations have used them in their annual reports.

What Are Nonprofit Financial Statements?

Nonprofit financial statements are formal records that detail your nonprofit’s financial activities.

They track how money is received, allocated, and retained.

Beyond helping your organization meet legal requirements, they also promote transparency and help you evaluate your performance.

Unlike for-profits, nonprofits don’t report profits. Instead, you’ll be reporting on net assets and how you use funds to advance your mission.

Why Do Nonprofits Need Financial Statements?

Nonprofits must comply with the IRS and file four financial statements to ensure they follow strict nonprofit regulations. Many of these statements are similar to what for-profit businesses file, but some significant differences exist.

Most nonprofits share these statements to be entirely transparent with their donors; often using these statements in their annual or impact reports. By sharing what funds you collect and how they’re spent, donors can see how their gifts support your nonprofit’s programs and beneficiaries.

Financial statements also give donors a better understanding of how the organization is doing.

Foundations require nonprofits to provide financial statements when they apply for grants. Major donors may also want to see financial statements before giving a significant gift.Generally, when a nonprofit shares more about its financial health, foundations and sponsors see that the nonprofit is financially viable and feel safer giving.

Financial statements also help you determine the future of your organization. They help board members better understand your nonprofit’s capacity for growth, too. Finally, they also enable leadership to find potential financial opportunities and ways to address financial concerns.

Bonus Resource: Watch this Webinar on Annual Reports for enhanced donor engagement.

The first and most desired financial statement is the statement of financial position. Nonprofits use this statement to share what their organization owns and what it owes.

The idea is to give an overall picture of your nonprofit at a specific time. It will also show the financial health of your organization. Your organization must add this statement when filing Form 990.

You’ll use the statement of financial position to list your assets, liabilities, and net assets.

Let’s have a look at what each element of this statement means.

1.1 Assets

Assets are what your organization owns. These can include office supplies and equipment, event supplies, cash, donations, grants, and property. You can also include intangible assets like copyrights, trademarks, and patents. In the end, you need to list these assets in order of liquidity.

1.2 Liabilities

Liabilities are what your nonprofit owes. Liabilities include things like salaries, debt, and grants to other organizations. When listing your nonprofit’s liabilities, you must list them by when they must be paid and separated by current and long-term liabilities.

Long-term liabilities are car loans and mortgages, whereas current liabilities cover accounts payable debt like salaries and immediate payments.

1.3 Net assets

The IRS does not allow charities to make a profit. Your nonprofit’s liabilities and assets must balance. Net assets are any assets left over after subtracting your liabilities.

Your net assets can be from the current and previous operating years and include anything that holds value. Nonprofits don’t have to list net assets line by line.

At times, supporters will give donations stipulating that they can only be used on a specific project or program. The net assets on your statement of financial position are where your organization must list these restrictions.

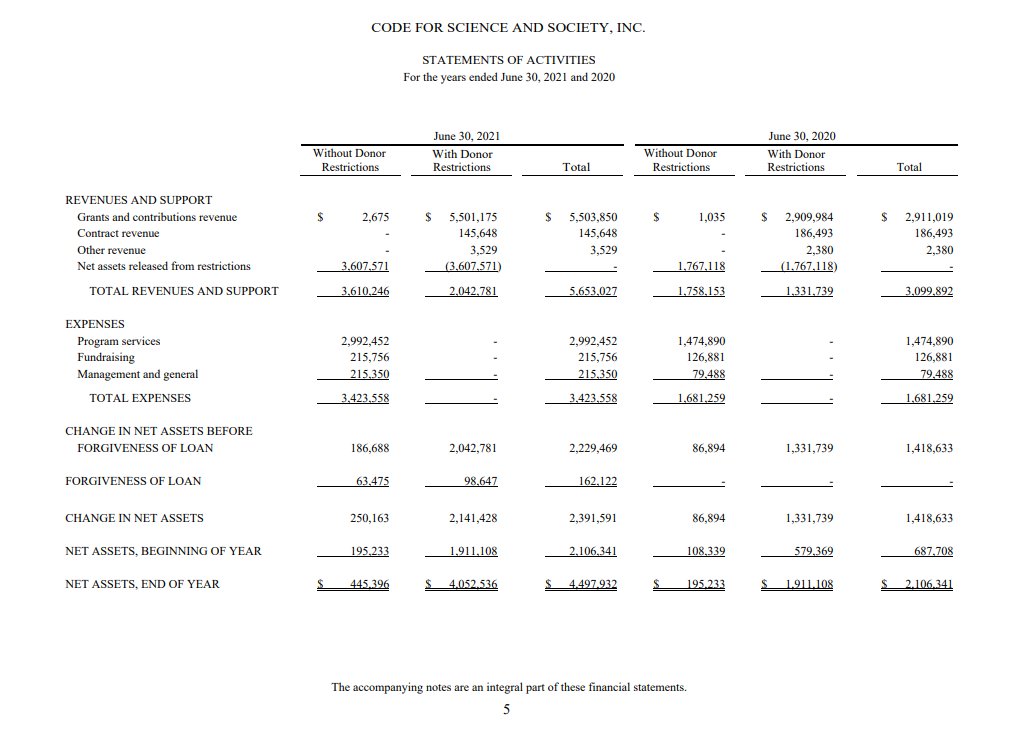

2. Statement of Activities

Nonprofits use the statement of activities to review changes to their net assets and show revenue and expenses over the accounting year. In other words, it tracks your nonprofit’s financial performance and shows how you’ve used your funds to support your mission.

The statement follows a simple formula:

Revenues – expenses = change in net assets

You can break down your net assets into two main categories: with donor restrictions and without donor restrictions. Following Generally Accepted Accounting principles (GAAP) or International Reporting Standards (IFRS), your organization should label these two types of assets clearly.

Let’s take a look at an example from the Code for Science & Society to help you get a better understanding:

One important difference between nonprofit and for-profit reporting in this statement is the use of gross receipts instead of gross sales. Essentially, gross receipts refer to the total amount your nonprofit brings in from all sources – donations, memberships, grants, etc.

Your nonprofit can record revenue and expenses with a cash or accrual method. Most nonprofits use the accrual method, though, because it records revenue when it’s earned rather than when it’s received.

3. Statement of Cash Flow

The statement of cash flow shows how cash moves in and out of a nonprofit. Board members and other leaders can use this statement for better insight into how much is available to pay expenses.

Here’s what it looks like in the Oxfam 2024 financial report:

The statement of cash flow is broken down into three sections.

3.1 Operating

Operating revenue includes funds from donations, ticket sales, product sales, etc. Operating expenses are your employees’ salaries and the amount spent on equipment and supplies.

3.2 Investing

Investing revenue is the amount of interest you can make from investments. Investing expenses are the purchases of long-term investments and any payments on long-term investments like buildings, land, equipment, etc.

3.3 Financing

Finally, financing revenue comes from the earnings and interest earned on your financial activities and savings. Financial expenses include the interest paid on financial loans.

4. Statement of Functional Expenses

The statement of functional expenses gives donors more details on how the organization spends funds. The IRS also requires nonprofits to include this statement when filing Form 990.

Did you know that websites like Charity Navigator and GuideStar use this report to rate your organization? In other words, it’s very important where public perception is concerned.

Your nonprofit must include natural and functional classifications for all expenses. Organizations will separate these expenses by programs, fundraising, and management. With each of these, include salaries, events, administrative costs, etc.

Habitat for Humanity depicts their 2024 Functional Expenses on this page of their report in great detail:

How to Prepare Financial Statements for Your Nonprofit

Some basic accounting knowledge and good attention to detail will come in handy when preparing your nonprofit’s financial statements, but here are a few steps to help you get started:

Compile Financial Data: Gather information on donations, revenue, grants, salaries, program costs, and other transactions. In other words, any transaction made by or to your organization. Having a good financial management plan in place will make this process a lot easier!

Choose an Accounting Method: As we mentioned before, most nonprofits use the accrual method.

Use Fund Accounting: Be sure to track restricted and unrestricted funds separately to meet donor requirements and reporting criteria.

Prepare the Four Key Statements: Create the statements we discussed above.

Review and Share: Ask your board or finance team to review your statements. You can even have them checked by an independent auditor. Then, publish them on your website or include them in your annual report.

3 Great Examples of Nonprofit Financial Statements

As we mentioned earlier, many nonprofits use these financial statements in their annual reports to show transparency and build trust in their organization.

The following three nonprofits have included financial statements in different ways.

1. Feeding America

Every year, Feeding America puts together a comprehensive annual report that’s as specific as it is well-designed. Apart from all the relevant financial statements, you’ll also find interesting statistics and notable achievements the organization made throughout the year.

Top tip: Take a page out of Feeding America’s book and Include your financial statement in your annual report. Why? It gives your supporters a closer look at your important work beyond the nitty-gritty accounting details.

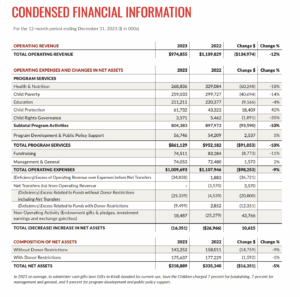

2. Save the Children

Like Feeding America, Save the Children also includes financial statements in their annual reports. However, their financial information is much more condensed here.

The rest of the organization’s 2023 report is packed with interesting insights, quotes from individuals they’ve helped, and more. If your nonprofit is just starting out, use this annual report as inspiration.

Even though the statement in the annual report is simplified, you’ll still find fully audited yearly financial statements on the organization’s website – plus all their Form 990 submissions dating back from 2011.

3. Heliconia Scholarship Foundation

Heliconia Scholarship Foundation shares a financial report with its donors instead of an annual report. This decision makes sense, since donors to a scholarship fund are likely concerned solely with financial details from this organization.

Compared with Feeding America and Save the Children, the financial statements used in this report are easier to follow and provide fewer details.

On the other hand, they share how these funds support students throughout their education. The scholarship foundation’s details fit well with what donors expect to hear from the organization.

Key Financial Ratios for Nonprofits

As you now know, your financial statements tell a story – but financial ratios help you analyze it! Here are four important ratios to track:

1. Program Efficiency Ratio

Formula: Program Expenses ÷ Total Expenses

This metric is important because it shows how much of your spending goes directly to mission-related activities. Most nonprofits would agree that a ratio above 75% is efficient.

2. Fundraising Efficiency Ratio

Formula: Fundraising Expenses ÷ Total Donations Raised

This metric shows how much you raise for every dollar spent on fundraising efforts. A ratio of 5:1 is generally considered healthy – but it also depends on the size of your organization.

This metric indicates how long your nonprofit can operate if it stops generating income. To be safe, you should aim for a 3-6 month reserve.

4. Current Ratio/Working Capital Ratio

Formula: Current Assets ÷ Current Liabilities

This ratio measures your short-term financial health and ability to meet obligations.

Final Thoughts

Nonprofits must file financial statements with the IRS to follow compliance laws, which is not the only reason they should include these activities. Providing detailed financial statements and an explanation of how these details help the organization and its beneficiaries strengthens relationships with donors and opens up opportunities to solicit significant gifts.

If you’re starting a nonprofit or have started one already and are in need of knowing the ropes, check out our Nonprofit Blog. You’ll also find a plethora of other insightful topics including fundraising ideas, tips, donor management and communication guides, downloadable resources, and more over there. Subscribe to our monthly newsletter if you want us to send you the best Donorbox resources directly to your inbox.

Donorbox is an affordable and simple-to-use online fundraising tool with powerful fundraising features such as Recurring Donations, Crowdfunding, Peer-to-Peer, Events, Memberships, and more. You can also manage donors, send them automated donation receipts, add offline donations, let donors login and manage their accounts themselves, and more on Donorbox. Learn more on our website.

We have designed a success package for nonprofits that are willing to take their fundraising to the next level. Check out Donorbox Premium – talk with expert fundraising coaches, get priority tech support, have an account manager to guide you at all times, and discover powerful tools. Pricing is personalized for each organization. Book your demo today!

Disclaimer: By sharing this information we do not intend to provide legal, tax, or accounting advice, or to address specific situations. The above article is intended to provide generalized financial and legal information designed to educate a broad segment of the public. Please consult with your legal or tax advisor to supplement and verify what you learn here.

Kristine Ensor is a freelance writer with over a decade of experience working with local and international nonprofits. As a nonprofit professional she has specialized in fundraising, marketing, event planning, volunteer management, and board development.